Capital Market

Are we ready for the newcomers?

Alex K. Mathews, Research Head

The currency derivative segment has added three new currency pairs from this month onwards namely Euro, Great Britain Pound and Japanese Yen. We have seen volumes building up from $ 60 million at the time of USD/INR introduction to $ 600 million as on January 19, 2010 indicating the increased participation in this segment. The new pairs include GBP/INR (GBP- Great Britain Pound), YEN/INR and EURO/INR and these newcomers have started to trade on our exchanges from February 01, 2010 onwards. Now that the new currencies have started to trade on our exchanges as well, exporters and importers who invoiced their receivables or payables in Euro and were forced to hedge those positions in Dollars, would now not only be able to hedge directly but can also price their products and services in a better manner.

But as these currency pairs are in our country for the first time, we should know what are the factors that affect their movements, their relationships with other currencies and also with USD/INR. To be smart and informed while trading in forex, one should have the necessary data and tools as well to make the right decision, such as the US Dollar Index and the Commitment of Traders Report (C.O.T Report).

US Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies. The basket of currencies includes Euro, Japanese Yen, Pound Sterling, Canadian dollar, Swedish krona and Swiss Franc. It represents the relationship between the US Dollar and these six currencies. In the index, Euro has the highest weightage of 57.6% followed by Yen 13.6%, British pound 11.9%, Canadian dollar 9.1%, Swedish krona 4.2% and Swiss Franc 3.6%. The dollar index was started in the year 1973. The dollar index is quoted in New York Board of Trade and is updated whenever US dollar markets open. They can be traded as a futures contract on the Inter Continental Exchange, in exchange traded funds, options and mutual funds. As Euro has the highest weightage in the index, a major event in the Euro zone would have a major effect on the US dollar index when compared to the other index members.

Another factor is the Commitment of Traders Report or the C.O.T Report. It is published every Friday and it measures the net long and short positions taken by traders in the futures market. It is a great resource to gauge the market sentiment of the big players because of their large positions and helps small investors to be on the safer side while taking positions. The C.O.T report allow us to quickly sort currency positions by group, commercial, large traders and small speculators in ascending and descending order. This will help us to quickly identify breakouts or overbought and oversold markets by group, as a percentage of the current net positions when compared to various historical time frames.

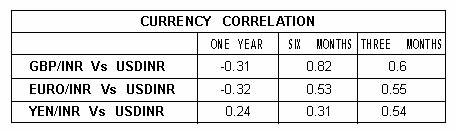

From the trading point of view, the correlation between USD/INR and the new entrants show some interesting facts. One year historical data of USD/INR and others show that GBP/INR and EURO/INR have negative correlation while YEN/INR shows very low correlation. Six month and three month correlations are showing some positive trends. The following table shows the correlation between the new pairs and the existing USD/INR.

The initial signs are good with Euro futures clocking 10 times more in turnover when compared with the turnover of dollar futures on its debut day. The Euro futures contract recorded a total turnover of Rs 1173 crore on NSE compared with Rs 45 crore and Rs 59 crore turnover recorded by futures contract in Yen and Pound respectively. From the impressive performance on the first day, the newcomers are expected to move forward at a smart pace.